Power purchase agreements (PPAs) are complex products and understanding the correct accounting treatment for them can be difficult.

How PPAs are dealt with for accounting purposes can significantly impact corporate balance sheets and profit and loss (P&L), potentially introducing volatility into company earnings.

This short blog outlines some of the key approaches and tests to consider when looking at PPA accounting from the point of view of a PPA off-taker. It also includes some useful links and various guidance documents from across the industry.

It likely goes without saying, but this guidance – as detailed as some of it is – is no substitute for professional advice.

Introduction

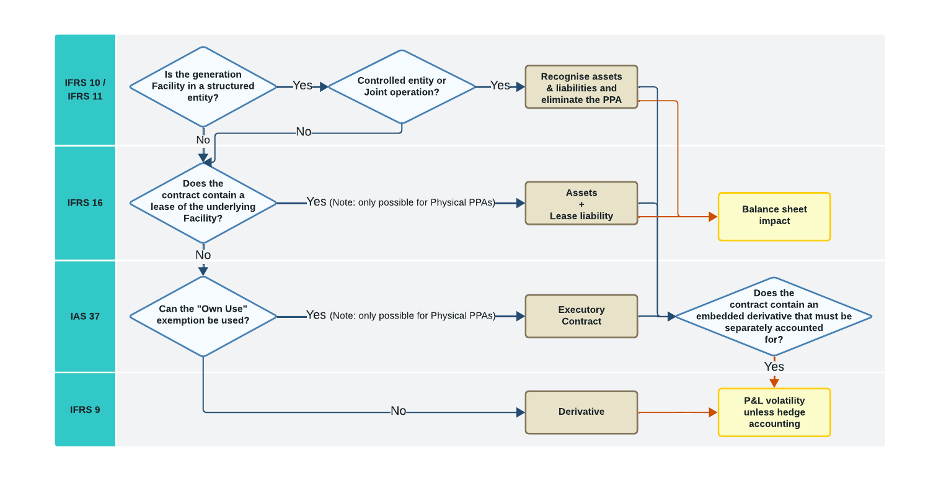

Assuming the customer does not have control over the project supplying the power, there are essentially three ways to account for a clean energy PPA. To decide on the appropriate approach, accountants will follow a decision tree – as per the graphic below.

The first question is to ascertain if the contract can be interpreted as a lease, thus falling under leasing accounting, as set out in the IFRS 16 accounting standard.

Whether or not it contains a lease, some PPAs are considered to be financial instruments. This means that they need to be accounted for under derivative accounting (IFRS 9).

If none of these criteria are met, the PPA falls under executory contract accounting (IAS 37). This is the most straightforward and preferable accounting treatment.

Now let’s look at which accounting standard is likely to be most appropriate, and their respective pros and cons.

Lease accounting

A lease is defined by IFRS 16 as a “contract or part of a contract that conveys the right to use an asset for a period of time in exchange for consideration”.

A contract is treated as a lease if:

- there is a specific asset identified;

- the customer purchases substantially all the output of an asset;

- the customer has the right to direct how and for what purpose the asset is used throughout the period of use.

Determining the final criteria requires careful consideration of the contract terms, but typically for a PPA that has predetermined operation (e.g., no right for the customer to impose curtailment), the test for a right to direct use comes down to whether the customer operates the asset itself or has been involved in the asset’s design.

The implications of lease accounting treatment are that, if a PPA is accounted for as a lease, it must be recognised as a right-of-use asset and appear as a liability on the balance sheet. Such accounting can have significant impacts on the offtaker’s financial statement, EBITDA and debt-to-equity and interest cover ratios. This, in turn, can have impacts on debt covenants and management incentive schemes.

Derivative accounting

Whether the PPA implies a lease of the assets or not, the next stage is to consider whether it effectively incorporates a derivative. If it does so, accounting rules usually require these embedded derivatives to be accounted for as if they were a free-standing contract.

Determining if a host contract contains an embedded derivative can be challenging. One indicator is that its value is based on an underlying variable (e.g., electricity prices). Others include the contract requiring no (or a relatively small) initial net investment, and that it is settled at a point in the future.

If the PPA is considered a derivative, it falls under IFRS 9, and must be fairly revalued in every reporting period, with any changes to its value recorded as a profit or a loss. This can introduce volatility into the offtaker’s P&L, even though there may be no actual financial impact (because any ‘loss’ on the PPA would be balanced by an offsetting ‘profit’ in the offtaker’s actual electricity bill).

Own-use exception

However, an exception from IFRS 9 accounting may be applicable if the purpose of the PPA contract is to directly provide electricity for the customer’s use. This would allow for the PPA to be treated as a normal course executory contract (see below).

The conditions to qualify for the own-use exception are particularly strict, requiring actual physical delivery and consumption by the customer of all electricity purchased under the contract. This requirement rules out all virtual PPA structures, as well as physical PPAs where there is net settlement, or any sale of excess generation.

Very careful consideration of the requirements is necessary before applying the exception. The IFRS is currently undergoing a process to amend the standards relating to the application of the own-use exemption, having accepted in June 2023 that the current requirements do not provide an adequate basis to determine the appropriate accounting for certain PPA scenarios submitted to it.

Hedge accounting

If the PPA doesn’t qualify for an own-use exemption, there is another accounting treatment option. If certain conditions are met, a PPA can be designated to be in a cash-flow hedging relationship and can be accounted for as other comprehensive income. This results in lower volatility in P&L from the recognition of changes to the PPA’s fair value.

An important requirement for designation as a hedging instrument is for the hedged item to be highly probable in all cases, and therefore there may be some effectiveness from the hedge. Assessing the correct application of the highly probable criteria requires thorough consideration by professional advisors.

Executory contract accounting

If the PPA does not contain a lease nor a derivative, it can be accounted for as a regular supply contract, where expenses are included in the income statement based on the costs attributable to the power delivered to, and consumed by, the off-taker in its course of business.

Under this treatment, the PPA is accounted for using IAS 37. This is the most preferable treatment for corporates, as it avoids the significant balance sheet impact under lease accounting, or the increased P&L volatility under IFRS 9 accounting.

Summary

Accounting for PPAs is by no means a simple task. The links below provide more in-depth information and advice, but careful consideration by professionals is necessary to ensure the correct treatment. If you’d like further information on this pretty complex area then please do reach out to the team at Squeaky.

Appendix: Useful Links and Guidance

IFRS accounting outline for Power Purchase Agreements (WBCSD)

Accounting for Green/Renewable Power Purchase Agreements from the Buyer’s Perspective (PwC)

Energy Transition: lease considerations for Power Purchase Agreements (EY)

Accelerate Accounting for Power Purchase Agreements (Deloitte)

Application of the “Own Use” Exemption for IFRS 9 (IFRS Amendment Process)

https://www.iasplus.com/en/meeting-notes/ifrs-ic/2023/june/ifrs-9